Understanding Advance Tax Rules: Payment Obligations, Exemptions, and Quarterly Deadlines Explained

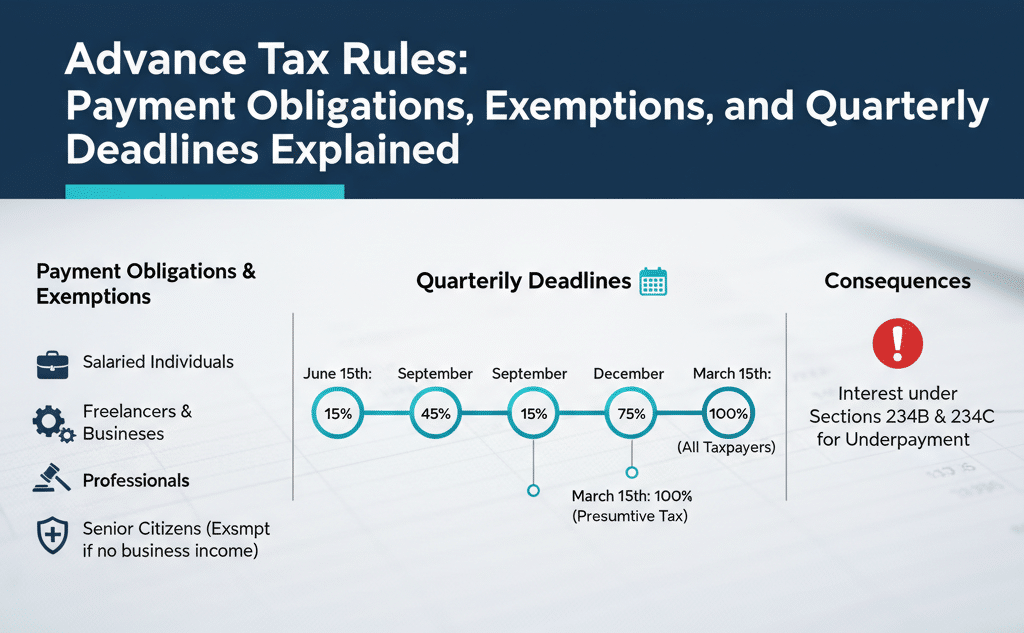

If your net income tax liability surpasses Rs 10,000 in a financial year, you are obligated to pay advance tax in four installments, as mandated by the Income Tax Act of 1961. This requirement applies to most taxpayers, though certain exemptions exist for specific groups. Notably, senior citizens and salaried individuals with tax liabilities fully covered by TDS are exempt from advance tax payments, even if their total tax liability exceeds the threshold.

Understanding Advance Tax Payments

Advance tax is a system that requires taxpayers to pay their estimated tax liability in advance, rather than waiting until the end of the financial year. According to Section 211 of the Income Tax Act, individuals must make these payments in four quarterly installments. The deadlines for these payments are set for June 15, September 15, December 15, and March 15 of the financial year. However, taxpayers under the presumptive taxation scheme can opt to make a single consolidated payment by March 15.

Chartered Accountant Bharat D Sarawgee from NRI Nivesh highlighted that resident senior citizens aged 60 and above are completely exempt from advance tax if they do not earn income from business or profession. This exemption holds true even if their total tax liability exceeds Rs 10,000. Additionally, salaried individuals whose entire tax liability is covered by TDS are also exempt, provided they do not have any other taxable income apart from their salary.

Exemptions for Certain Income Sources

The Income Tax Act recognizes that some income sources cannot be accurately estimated in advance. In such cases, taxpayers are permitted to pay advance tax on these incomes in the subsequent quarter after the income is actually earned. Common examples include capital gains from listed equity shares. Chartered Accountant Manas Chugh, head of regulatory services at Osgan Consultants, explained that individuals with specific income sources are exempt from paying advance tax upfront. Instead, they can settle their advance tax obligations in the next quarter when the actual income is realized.

The law specifies that advance tax for certain categories of income, such as capital gains, lottery winnings, and first-time business income, can be paid in the following quarter. This provision aims to protect taxpayers from incurring penal interest when precise calculations of advance tax liability are not feasible.

Advance Tax Deadlines for FY 2025-26

For the financial year 2025-26, the advance tax payment deadlines are set for June 15, September 15, December 15, and March 15. Taxpayers must adhere to these deadlines to avoid penalties. The advance tax payable is structured as follows: 15% of the net estimated tax liability is due by June 15, 45% minus any tax already paid by September 15, 75% minus any tax already paid by December 15, and 100% minus any tax already paid by March 15.

It is crucial to note that advance tax is only required if the net tax liability after accounting for TDS exceeds Rs 10,000. If the net liability falls below this threshold, taxpayers are not obligated to make advance tax payments. This system is designed to ensure that taxpayers meet their obligations while also providing relief to those with lower tax liabilities.

Observer Voice is the one stop site for National, International news, Sports, Editor’s Choice, Art/culture contents, Quotes and much more. We also cover historical contents. Historical contents includes World History, Indian History, and what happened today. The website also covers Entertainment across the India and World.